Domestic aluminum scrap prices followed primary aluminum higher this week, with the price center moving up significantly. As of December 4, the SMM A00 aluminum price closed at 22,020 yuan/mt, up 560 yuan/mt from last Thursday. The mainstream categories of aluminum scrap struggled to keep pace with the gains. Shredded aluminum tense scrap (including freight) closed at 18,400-18,900 yuan/mt (ex-tax), while baled UBC closed at 16,400-16,900 yuan/mt (ex-tax), with cumulative gains reaching 200-300 yuan/mt. On one hand, intensified year-end environmental protection measures and transport restrictions in Henan affected delivery efficiency. Meanwhile, some scrap utilization enterprises reported high inventories of profile scrap recycled during the peak season, but lacked sufficient orders on hand to hedge against raw material stocks, leading them to temporarily slow the procurement pace for profile scrap. On the other hand, supply of aluminum tense scrap remained tight. Some import traders in east China reported that imports fell sharply by 40%-60% due to persistently high LME aluminum prices. Regarding the price difference between primary metal and scrap, the price difference between A00 aluminum and shredded aluminum tense scrap closed at 1,749 yuan/mt on December 4, while the price difference for bare bright aluminum wire in Jiangsu was 891.3 yuan/mt. Aluminum scrap prices are expected to hover at highs next week, with the mainstream range for shredded aluminum tense scrap (including freight) forecast at 18,500-19,200 yuan/mt (ex-tax). The tight supply situation is difficult to change, with constraints on imports and recycling still present, providing a floor for prices. Demand side, the year-end push for annual targets by secondary aluminum producers and the inhibitory effect of high prices are intertwined, leading to cautious purchasing by extrusion and rolling scrap utilization enterprises who are wary of high prices. The price trend of primary aluminum serves as the core guide. Coupled with the impact of environmental protection-driven production restrictions and transport constraints in central China, market sentiment is cautious. Overall, the tug-of-war between sellers and buyers continues, requiring close monitoring of primary aluminum price fluctuations, environmental protection policies, and downstream procurement pace, while remaining vigilant against the risk of a pullback from highs.

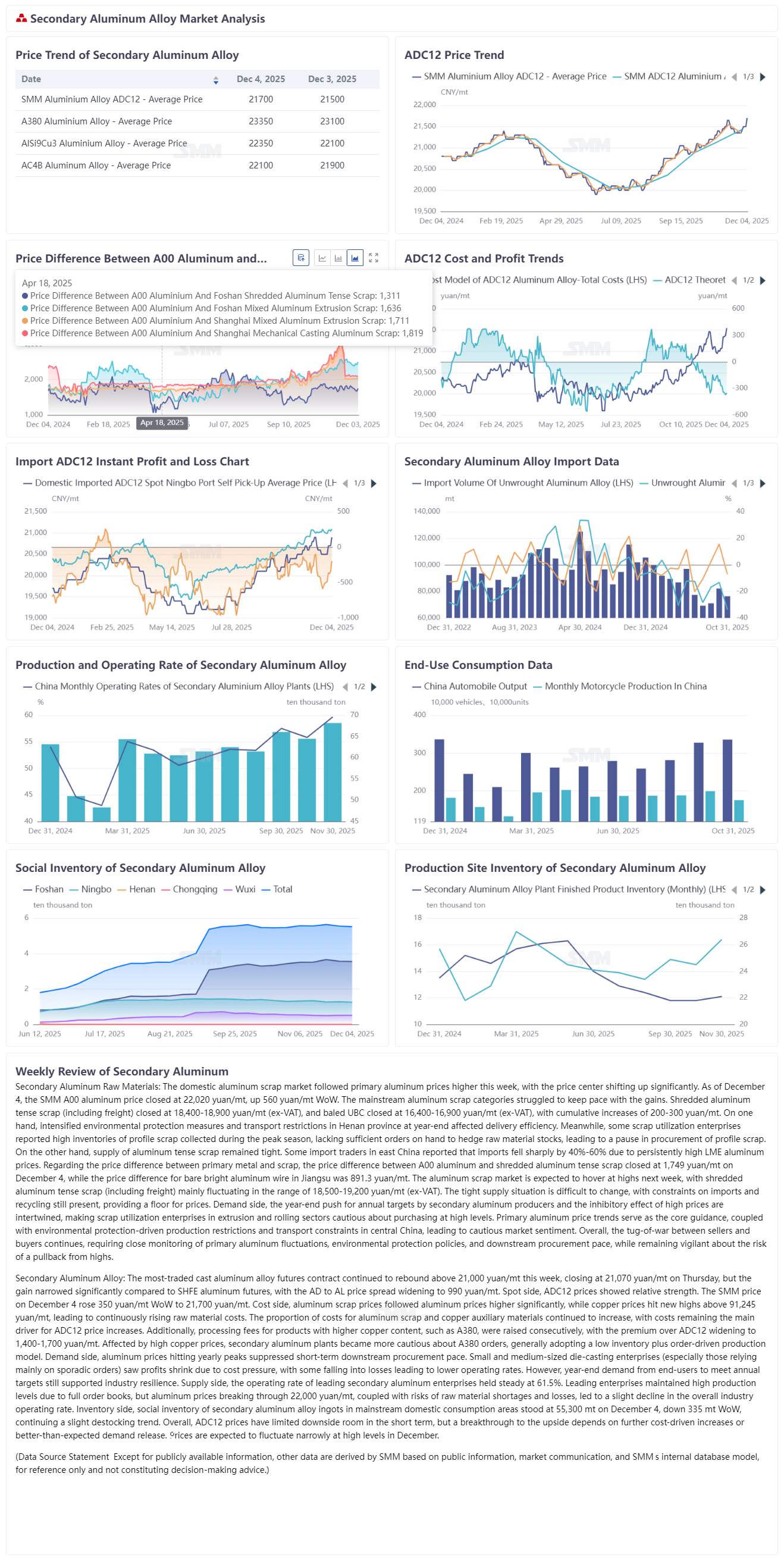

The most-traded cast aluminum alloy futures contract continued its rebound above 21,000 yuan/mt this week, closing at 21,070 yuan/mt on Thursday. However, the gain was significantly narrower than that of SHFE aluminum futures, and the AD-AL price spread widened to 990 yuan/mt. In the spot market, ADC12 prices showed relative strength. The SMM price on December 4 rose 350 yuan/mt from last Friday to 21,700 yuan/mt. Cost side, aluminum scrap prices rose sharply following aluminum prices, while copper prices reached new highs above 91,245 yuan/mt, leading to continuously rising raw material costs. The cost share of aluminum scrap and copper auxiliary materials continued to increase, with cost remaining the main driver of the rise in ADC12 prices. Additionally, processing fees for products with higher copper content, such as A380, were raised successively, with the premium over ADC12 widening to 1,400-1,700 yuan/mt. Affected by high copper prices, secondary aluminum plants became more cautious regarding A380 orders, generally adopting a low inventory + order-driven production model. Demand side, aluminum prices surging to their yearly peak inhibited short-term downstream procurement pace. Small and medium-sized die-casting enterprises (especially those relying mainly on sporadic orders) saw profits shrink due to cost pressure, with some falling into losses leading to a decline in operating rates. However, year-end demand from end-users pushing for annual targets still supports industry resilience. Supply side, the operating rate of leading secondary aluminum enterprises held steady at 61.5%. Leading enterprises maintained high production levels supported by full order books. However, aluminum prices breaking through 22,000 yuan/mt, combined with risks of raw material shortages and losses, led to a slight pullback in the industry's overall operating rate. Inventory side, social inventory of secondary aluminum alloy ingots in mainstream domestic consumption areas stood at 55,300 mt on December 4, down 335 mt from last Thursday, continuing a slight destocking trend. Overall, the downside room for ADC12 prices is limited in the short term, but a breakthrough to the upside depends on further cost-side pushing or better-than-expected demand release. Prices are expected to fluctuate narrowly at high levels in December.